With all the big changes in the current political and economic climate, it’s fair to say that millions of employees are feeling a very large and painful financial pinch.

In fact, in a survey of over 10,000 employees and 500 employers, 33% of employees said that financial worries are their biggest concern, after health (29%) and work-life balance (28%).

The independent research, the DNA of Financial Wellbeing 2017 from Neyber, shows how debt impacts millions of individuals, across pay-level, gender, age and region.

Household debt is rising

It tells us that, over the last 12 months, household debt has risen by 5.5% from £10,718 to £11,306, yet on the more positive side, employees seem to be managing their debt better than last year.

There’s been a 2% reduction in the number of repayment defaults and debt-related arrangements, dropping from 13% in 2016 to 11% this year.

With so much uncertainty in financial situations, it’s never been more important for training departments to use their abilities to support employees and the organisation.

Indeed, the Neyber survey showed that 82% of employers thought financial health is important to the organisation as a whole.

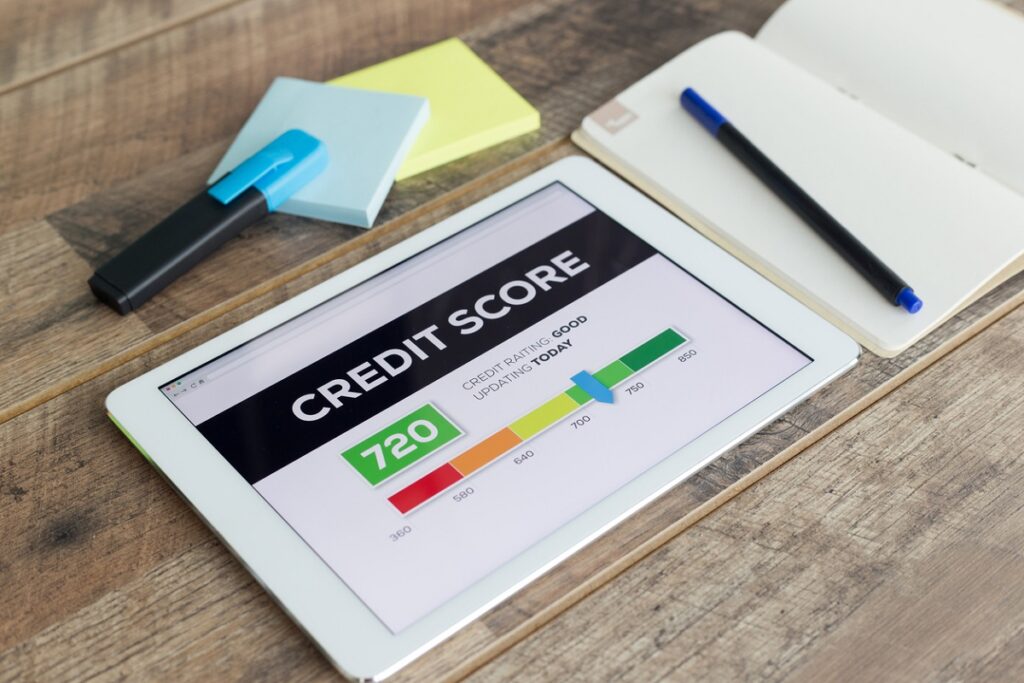

Credit scores often equal credit sores

There are many issues at hand – not least managing day-to-day finances, building financial resilience and fluctuating incomes – but we find a recurring issue is lack of knowledge about credit scores.

These are also known as credit files and credit reports. So many decisions made, financially-related and otherwise, can have a significant impact on someone’s credit score, often without them realising.

Educating employees on what makes a good credit score allows them to take advantage of the best financial offers and make better overall choices, whatever their current situation.

Yet with knowledge building, these issues are quite straightforward to minimise and negative effects significantly reduced.

The Neyber survey found that four in 10 employees surveyed had limited or no understanding of credit scores – and this rose to 54% for those aged 18-24. Of those aged 65 and over, 35% had the same limited knowledge.

Eighteen per cent admitted to not knowing what their score was and not regularly checking it – even more of a concern was that 8% of those aged 18-24 wouldn’t actually know where to go to check.

So, there is a considerable amount of knowledge building to help employees understand what they can do to help or hinder their credit score.

Little things make a big difference

Educating employees on what makes a good credit score allows them to take advantage of the best financial offers and make better overall choices, whatever their current situation.

This freedom of choice is vital, although perhaps subliminal, to feeling secure in managing day-to-day financial activity. It’s a positive tick in a long list of tick boxes.

There are things people do in every day situations that can surprise them when they learn these negatively impact their credit score.

Frequent moving, for instance – which is likely to affect younger people who rent and move around – will affect their credit score if they do not manage things properly. Incomplete address histories, when someone isn’t on the electoral roll, or frequent credit searches when switching utility providers are all noted on a credit file, can all bring a score down.

Understanding the nuances of APR – or an annual percentage rate – is also important. APR is the total cost of borrowing over a year and knowing rates helps people compare the costs of borrowing and understand the impact on payments.

It’s important to make APR as simple and digestible as possible, which, frankly, isn’t always easy to do. In general terms, the better someone’s credit score, the better the interest rate they’ll be offered, which helps ensure cheaper financial products.

The credit trap

With this, you can see why a credit trap builds for people who have less disposable income, earn less or have poor credit scores.

These mean they’ll be offered higher rates of interest, increasing their financial strain.

APR is the total cost of borrowing over a year and knowing rates helps people compare the costs of borrowing and understand the impact on payments.

There are so many things people shouldn’t do, but aren’t necessarily aware: don’t get drawn in by credit card offers, don’t spend on things they don’t need, especially younger people, as saving and having a good credit score, will ease their steps in the future – whether to purchase a home, get married or start a family.

I’d say that too many people spend money they haven’t earned, to buy things they don’t need, to impress people they don’t like.

Employers can help individuals take control

Building financial knowledge in employees is so helpful to their wellbeing. It is far better, for every individual, to understand, to be realistic and take control.

Indeed, when people are under financial pressure – they often are so blinded by the current need that the actual day-to-day cost is the least of their worries.

Often they are just relieved to be accepted and don’t really understand the impacts of higher rates. Communication and education are there to help every individual.

With all the big changes in the current political and economic climate, it’s fair to say that millions of employees are feeling a very large and painful financial pinch.

In fact, in a survey of over 10,000 employees and 500 employers, 33% of employees said that financial worries are their biggest concern, after health (29%) and work-life balance (28%).

The independent research, the DNA of Financial Wellbeing 2017 from Neyber, shows how debt impacts millions of individuals, across pay-level, gender, age and region.

Household debt is rising

It tells us that, over the last 12 months, household debt has risen by 5.5% from £10,718 to £11,306, yet on the more positive side, employees seem to be managing their debt better than last year.

There’s been a 2% reduction in the number of repayment defaults and debt-related arrangements, dropping from 13% in 2016 to 11% this year.

With so much uncertainty in financial situations, it’s never been more important for training departments to use their abilities to support employees and the organisation.

Indeed, the Neyber survey showed that 82% of employers thought financial health is important to the organisation as a whole.

Credit scores often equal credit sores

There are many issues at hand – not least managing day-to-day finances, building financial resilience and fluctuating incomes - but we find a recurring issue is lack of knowledge about credit scores.

These are also known as credit files and credit reports. So many decisions made, financially-related and otherwise, can have a significant impact on someone’s credit score, often without them realising.

Educating employees on what makes a good credit score allows them to take advantage of the best financial offers and make better overall choices, whatever their current situation.

Yet with knowledge building, these issues are quite straightforward to minimise and negative effects significantly reduced.

The Neyber survey found that four in 10 employees surveyed had limited or no understanding of credit scores – and this rose to 54% for those aged 18-24. Of those aged 65 and over, 35% had the same limited knowledge.

Eighteen per cent admitted to not knowing what their score was and not regularly checking it – even more of a concern was that 8% of those aged 18-24 wouldn’t actually know where to go to check.

So, there is a considerable amount of knowledge building to help employees understand what they can do to help or hinder their credit score.

Little things make a big difference

Educating employees on what makes a good credit score allows them to take advantage of the best financial offers and make better overall choices, whatever their current situation.

This freedom of choice is vital, although perhaps subliminal, to feeling secure in managing day-to-day financial activity. It’s a positive tick in a long list of tick boxes.

There are things people do in every day situations that can surprise them when they learn these negatively impact their credit score.

Frequent moving, for instance – which is likely to affect younger people who rent and move around - will affect their credit score if they do not manage things properly. Incomplete address histories, when someone isn’t on the electoral roll, or frequent credit searches when switching utility providers are all noted on a credit file, can all bring a score down.

Understanding the nuances of APR – or an annual percentage rate – is also important. APR is the total cost of borrowing over a year and knowing rates helps people compare the costs of borrowing and understand the impact on payments.

It’s important to make APR as simple and digestible as possible, which, frankly, isn’t always easy to do. In general terms, the better someone’s credit score, the better the interest rate they’ll be offered, which helps ensure cheaper financial products.

The credit trap

With this, you can see why a credit trap builds for people who have less disposable income, earn less or have poor credit scores.

These mean they’ll be offered higher rates of interest, increasing their financial strain.

APR is the total cost of borrowing over a year and knowing rates helps people compare the costs of borrowing and understand the impact on payments.

There are so many things people shouldn’t do, but aren’t necessarily aware: don’t get drawn in by credit card offers, don’t spend on things they don’t need, especially younger people, as saving and having a good credit score, will ease their steps in the future - whether to purchase a home, get married or start a family.

I’d say that too many people spend money they haven’t earned, to buy things they don’t need, to impress people they don’t like.

Employers can help individuals take control

Building financial knowledge in employees is so helpful to their wellbeing. It is far better, for every individual, to understand, to be realistic and take control.

Indeed, when people are under financial pressure - they often are so blinded by the current need that the actual day-to-day cost is the least of their worries.

Often they are just relieved to be accepted and don't really understand the impacts of higher rates. Communication and education are there to help every individual.